Source: USDA

Comparing Annual Inflation Rates in 2023 and 2024

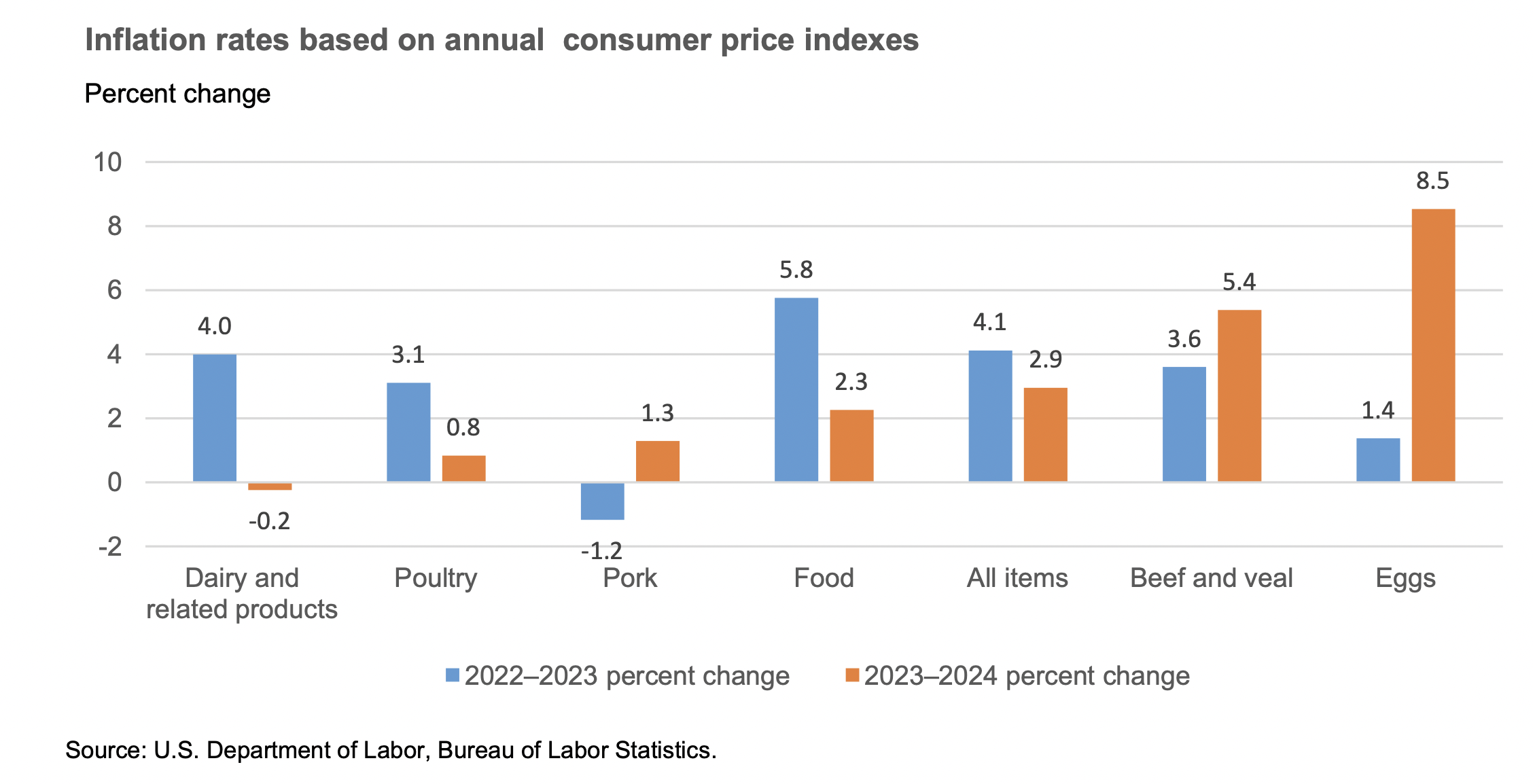

The Department of Labor’s Bureau of Labor Statistics released its annual Consumer Price Index, CPI, for 2024 on January 15, 2025. The chart below compares inflation rates in 2023 and 2024 for overall prices, food in general, and selected animal product groups. There are seven items in the chart below.

Inflation was lower in 2024 than in 2023 for four of the seven. In 2023 inflation was highest for food, at 5.8 percent, and for all-items at 4.1 percent. Dairy and related products had the lowest inflation rate between 2023 and 2024; their index decreased by 0.2 percent. The index for poultry increased only 0.8 percent, and for pork 1.3 percent. In 2024 food price inflation, 2.3 percent, was lower than the all-items inflation of 2.9 percent. The CPI for beef and veal increased by 5.4 percent in 2024, while eggs increased 8.5 percent.

Summary

Milk production for 2024 is lowered from last month, with lower estimates for milk cow

inventories and lower expected milk per cow ensuing from the most recent Milk Production

report. The all-milk price estimate for 2024 is $22.60 per hundredweight (cwt), $0.05 lower than last month’s forecast. With changes in the 2024 estimates for dairy cow inventory, the forecast for the average number of cows in the first half of 2025 is revised downward; however, the rounded 2025 average forecast for the dairy herd is unchanged at 9.390 million head. Compounded by a downward revision of 85 pounds in milk production per cow, the 2025 annual forecast for milk production has been lowered 0.8 billion pounds to 227.2 billion pounds. With higher price forecasts for dairy products in 2025, the forecast for the Class III and Class IV milk prices have been also revised upward. The all-milk price forecast for 2025 is $23.05 per hundredweight, $0.50 higher than last month’s forecast.

by: Angel Terán and Adriana Valcu-Lisman

Recent Wholesale Dairy Product Prices

Wholesale dairy product prices reported in the USDA National Dairy Products Sales Report

(NDPSR) increased from the week ending December 7, 2024, to the week ending January 4, 2025. The price for 40-pound blocks of Cheddar cheese rose 5.56 cents per pound, while 500- pound barrels (adjusted to 38-percent moisture) increased 4.52 cents per pound. The wholesale price for butter, nonfat dry milk (NDM), and dry whey rose by 3.25 cents, 0.86 cents, and 9.32 cents per pound, respectively.

For the trading week ending January 10 at the Chicago Mercantile Exchange (CME), the spot prices for Cheddar cheese 500-pound barrels and 40-pound blocks averaged $1.8655 and $1.8975 per pound, respectively. CME spot prices for NDM, butter, and dry whey averaged $1.3670, $2.5900, and $0.7415 per pound, respectively.

From November to December 2024, most Oceania and Europe average export prices2 reported by USDA Dairy Market News (DMN) decreased. The exception was the Western Europe export price for dry whey, which increased by a penny per pound. According to DMN, the world export demand for European dry whey remains active, as its price remains more competitive than U.S. dry whey.

Recent Dairy Supply and Use Data

According to the most recent Milk Production report published by the USDA, National

Agricultural Statistics Service (NASS), in November 2024, estimated milk production in the

United States was 17.875 billion pounds (596 million pounds per day), a reduction of 6 million pounds per day compared to November 2023 (-1.0 percent). NASS estimates the number of dairy cows in November to be 9.365 million head, 5,000 fewer than the previous month, and 20,000 more cows than in November 2023. The milk per cow estimate for November is 1,909 pounds, 23 pounds per cow less than in November 2023.

The average feeding costs were lower in November 2024 compared to a year ago, while the

average farmgate milk price was higher. According to the most recent NASS Agricultural Prices report, in November the corn price was $4.07 per bushel, $0.59 down from 2023, while the alfalfa hay price was $165.0 per short ton, $44.0 lower than November 2023. During the same period, the soybean meal price (reported by USDA, Agricultural Marketing Service) averaged $316.2 per short ton, down $148.1 from November 2023. The all-milk price in November averaged $24.20 per hundredweight (cwt), $2.60 higher than November 2023. The milk-feed ratio reported by NASS was estimated at 2.88 in November, up 0.78 points from November 2023. In November 2024, the farm milk margin above feed costs reported by the Dairy Margin Coverage program was estimated at $14.29 per cwt, $4.71 higher than last year.

Dairy cow slaughter has been relatively low throughout 2024. Weekly dairy cow slaughter in 2024 remains below 2023 levels but has been close to 2023 in the final weeks of 2024.

In November 2024, dairy product exports showed mixed results compared to the same month a year earlier. On a milk-fat milk-equivalent basis, exports totaled 944 million pounds, 128 million pounds higher than in November 2023. This increase was primarily driven by a rise in butter and cheese exports. Conversely, on a skim-solids milk-equivalent basis, dairy exports reached 3.6 billion pounds, a decline of 518 million pounds compared to November 2023. This decrease was mainly due to reduced exports of dry skim milk products, dry whey, and lactose.

Dairy imports in November were higher compared to a year ago. On a milk-fat basis, dairy

product imports totaled 887 million pounds, 225 million higher than November 2023. On a skim- solids basis, November imports totaled 596 million pounds, 57 million above November 2023. Dairy products with a notable year-over-year increase in November import volumes were butter, cheese, and infant formula.

In November, domestic use of dairy products showed mixed results compared to the same

month in 2023. On a milk-fat basis, domestic use amounted to 19.282 billion pounds, 474 million pounds higher than in November 2023. However, on a skim-solids basis, domestic use totaled 14.707 billion pounds, a decrease of 156 million pounds compared to the previous year. Year- over-year, the domestic use of butter and whey protein concentrate increased in November, while the use of cheese, nonfat dry milk, dry whey, and lactose declined.

In November 2024, the Restaurant Performance Index, which tracks the health of the U.S.

restaurant industry, increased by 0.8 percent compared to the previous month, suggesting that more people are dining out. According to the index, restaurants have been experiencing growth since October 2024, marking the first expansion of the year. If this trend of improving restaurant performance continues, it could benefit the dairy industry as well.

International Outlook for Dairy

On December 19, 2024, USDA, Foreign Agricultural Service (FAS) published the biannual

report Dairy: World Markets and Trade, covering an overview of the most recent developments and data on U.S. and global trade, production, consumption, and stocks. The report also includes projections for milk production for the major dairy producers.

Milk production in 2025 for Argentina, Australia, New Zealand, and the European Union (E.U) is expected to total 412.5 billion pounds, 1.2 billion pounds higher than last year’s production. Following a year with a sharp decline, Argentina’s milk production is projected to have the largest increase (+1.1 billion pounds) among the four countries due to favorable weather conditions, improved pasture availability, and favorable milk-to-feed price ratios, which may allow for improved milk per cow output. Australia’s milk production is expected to increase modestly by 0.2 billion pounds, supported by improved market conditions but constrained by dry conditions during late 2024 and poor pasture conditions in the southern and southwestern regions of the country. New Zealand’s milk production is also expected to increase by 0.5 billion pounds in 2025 as farmers expand herds and improve feed and management practices in response to higher global dairy prices. Among the highlighted dairy producers, the E.U.’s milk production is projected to decrease by 0.6 billion pounds as an expected decline in the dairy herd and Eurozone economic conditions may further challenge dairy farmers’ ability to expand milk production.

Dairy Estimates for 2024

Fourth-quarter and annual supply and use numbers in this report reflect Interagency Commodity Estimates Committee expectations because inventory, production, and trade data for December are not yet available.

Based on recent milk cow inventory and milk production data, the 2024 estimates for the

average number of milk cows, milk per cow, and milk production have been lowered from the previous forecast by 5,000 head, 50 pounds per cow, and 0.5 billion pounds, respectively. With these changes, the new 2024 estimates for these production projections are: 9.340 million head for the average number of milk cows, 24,170 pounds for milk per cow, and 225.8 billion pounds for milk production.

With relatively high November export volumes to South Korea, Mexico, and the Philippines,

the estimate for total 2024 dairy exports on a milk-fat basis are increased to 11.8 (+0.1) billion pounds. However, given the lack of price competitiveness for nonfat and skim milk powder products (NDM/SMP) and dry whey products, the estimates for exports on a skim-solids basis are revised downward to 49.1(-0.3) billion pounds. For 2024 imports, following recent strong butter imports from Ireland, the annual estimate on a milk-fat basis is increased to 9.5 (+0.3) billion pounds. However, on a skim-solids basis, the estimates for dairy imports are unchanged at 6.8 billion pounds.

The estimate for 2024 ending stocks on a milk-fat basis has been decreased to 13.2 (-0.5)

billion pounds, but the estimate on a skim-solids basis has been increased to 9.9 (+0.1) billion pounds. The estimates for 2024 domestic use have been adjusted to reflect recent data. On a milk-fat basis, the estimate for domestic use is 223.0 billion pounds, 0.1 billion higher than last month’s forecast. On a skim-solids basis, the estimate for 2024 domestic use is 182.4 billion pounds, 0.4 billion lower than the previous forecast.

While most dairy supply and use data are not yet available for December, complete 2024 prices data are available except for the all-milk price. For the year, the average wholesale prices for Cheddar cheese, dry whey, butter, and nonfat dry milk (NDM) were $ 1.8634, $ 0.4913, $ 2.8870, and $ 1.2420 per pound, respectively. Class III and IV milk prices averaged $18.89 and $20.75 per hundredweight (cwt), respectively. The all-milk price estimate for 2024 is $22.60 per cwt, 5 cents lower from last month’s forecast.

Dairy Forecasts for 2025

Following recent milk cow average inventory data, the forecast for the average number of cows has been lowered for the first half of the year. However, the national milking herd is projected to average 9.390 million head in 2025, unchanged from last month’s forecast when accounting for rounding. The forecast for milk per cow has been reduced by 85 pounds to 24,200 pounds. This reduction in forecasts reflects, in part, the lower-than-expected milk per cow in the fourth quarter of 2024 but also the expectation that the growth in milk components will likely balance out the lower-than-average growth in milk per cow.

With lower forecasts for dairy inventory as well as milk per cow, milk production for 2025 is

forecast at 227.2 billion pounds, about 0.8 billion pounds less than the previous forecast. NASS will issue its Cattle report on January 31 that will include milk cow inventory data along with dairy replacement heifer numbers. The report will give insight into the current state of the herd and will inform the outlook for much of 2025.

The dairy import forecasts for 2025 have been raised on a milk-fat basis to 9.3 billion pounds (+0.2 billion) but lowered to 7.3 billion pounds (-0.1 billion) on a skim-solids basis. While higher imports are expected for butter and cheese, lower imports are expected for casein products and milk protein concentrate. As domestic prices for butter and cheese are expected to remain competitive in world markets, the 2025 dairy export forecast on a milk-fat basis has been raised 0.2 billion pounds to 11.9 billion. Conversely, the lack of price competitiveness for dry whey and nonfat dry milk is expected to further limit dairy exports. Consequently, the 2025 dairy export forecast on a skim-solids basis has been revised downward to 49.1 (-0.40) billion pounds.

With a lowered forecast for milk production and higher projected prices for dairy products, the 2025 forecasts for domestic use are adjusted downward relative to last month’s projection. On a skim-solids basis, domestic disappearance has been lowered by 1.0 billion pounds to 184.1 billion pounds. On a milk-fat basis, 2025 domestic disappearance is forecast at 223.8 billion pounds, 1.3 billion pounds lower than the last forecast.

Based on recent movement in product prices, the 2025 average price forecasts for the major dairy products have been raised from the previous forecast. Wholesale price forecasts for Cheddar cheese, dry whey, butter, and NDM have been raised to $1.865 (+6.5 cents), $0.640 (+4.5 cents), $2.695 (+1.0 cents), and $1.340 (+4.0 cents) per pound, respectively.

The higher product price forecasts support upward revisions for milk class prices as follows: for Class III milk to $19.70 (+$0.90) per cwt, and for Class IV to $20.80 (+$0.40) per cwt. The all-milk price for 2025 is now forecast at $23.05, up $0.50 cents from last month’s forecast.

{kind=link}